Summary

Village Farms appears to be a greatly undervalued stock in the Agricultural Technology Sector.

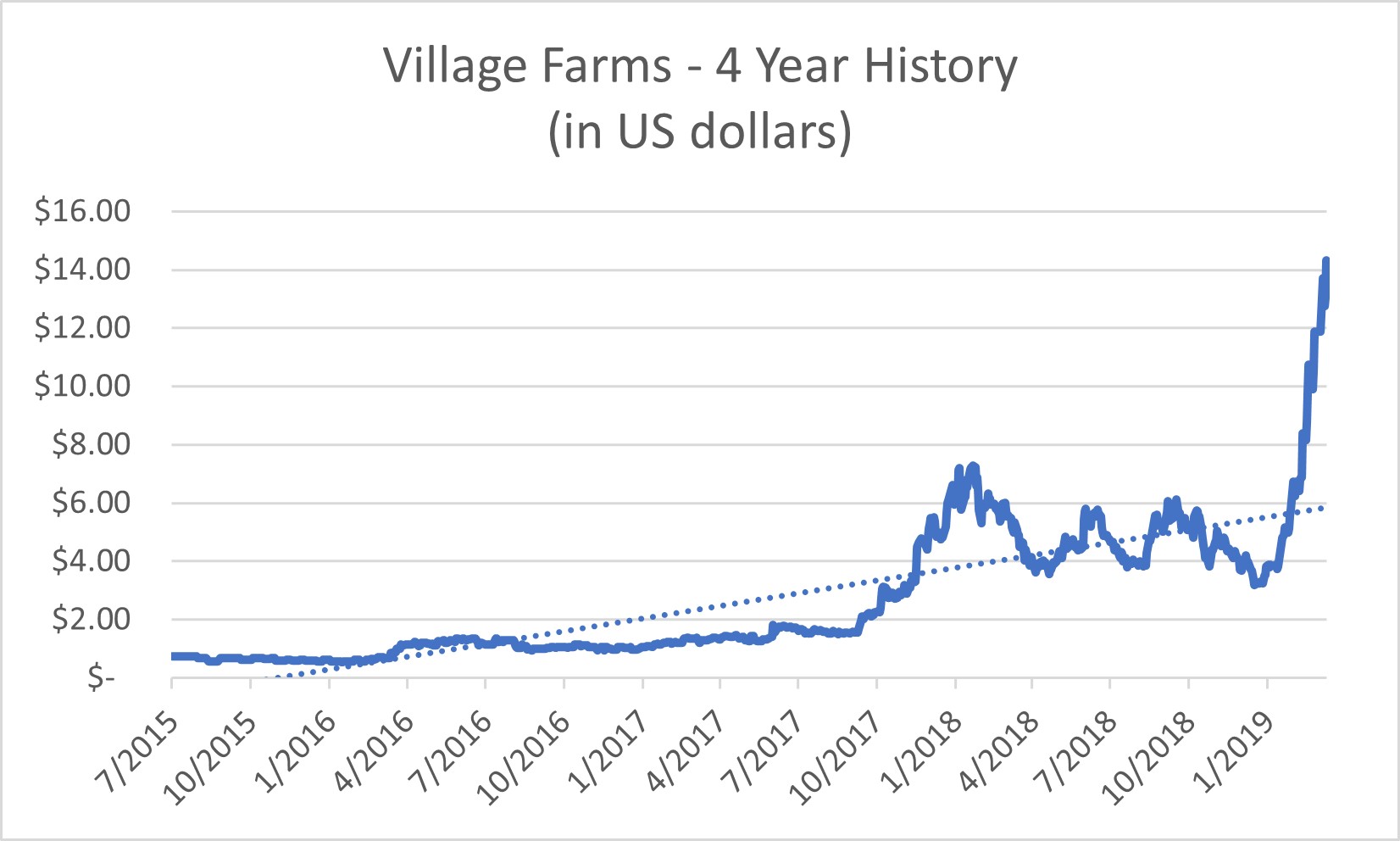

Village Farms has gained 34% in value since the initiating report from April 2016.

The recently announced JV with Emerald Health Therapeutics could be a major addition to Village Farms’ future earnings.

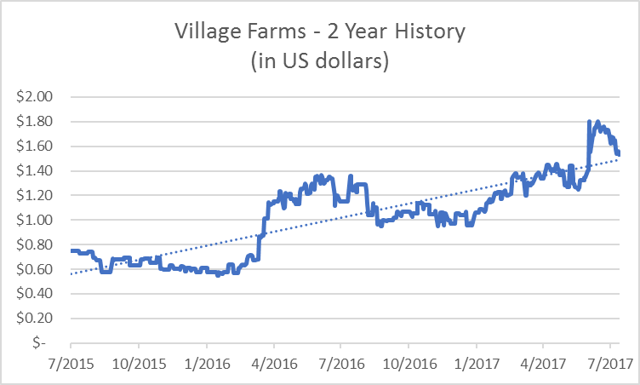

Village Farms (TSE: VFF) and (OTCQX:VFFIF) continues to offer an attractive entry for investors interested in the growing hydroponic sector. In April 2016, Village Farms: A Rare Undervalued Equity Investment Opportunity in the AgTech Sector outlined the prospects of this industry and correctly predicted the growth potential of Village Farms, an experienced greenhouse innovator; the stock has appreciated by over 34% since then with plenty more value ahead. It currently trades at $1.53 USD and should soon be trading above $2.50 with a target of $4.00 by the time it releases its 2017 annual report. The Company’s recent JV announcement with Emerald Health Therapeutics (OTCQX:EMHTF) to expand into the cannabis industry has furthered the significant upside potential of this stock and what could become a greenhouse powerhouse; one that would be trading far above the $4 per share we are targeting.

Agriculture Technology Industry Updates – Private Market

Investor demand has continued to build on the increased levels reached a few years ago. A sector that was once a $500 million-a-year allocation has become a $1 billion-a-year one with another $2 billion+ of capital put into the AgTech sector in 2015 and 2016. PE investments in the industry include NOVACAP’s investment in Mucci Farms (previously fined $1.5 million for product mislabeling), Catalyst Investors/WP Global Partners/NGEN Partners financing of Bright Farms and Avrio Ventures investment in Sun Select.

Agriculture Technology Industry Updates – Public Market

Most of the comparable companies remain private. The April 2016 report highlighted two public investment opportunities in this sector and found that “TerraTech appears overvalued while Village Farms appears greatly undervalued given their valuations and production capacities”.

*** The projections were correct. TerraTech (OTCQX: OTCQX:TRTC) is trading a couple cents below its April 2016 share value but has gone from a market cap of 22.8x Book Value to 3.3x; over that same period, Village Farms has gained 34% in value. The Company is still only trading at 1.1x Book Value, an improvement from 14 months ago (0.7x Book Value), but Village Farms remains undervalued.

Village Farms International – Summary Business Overview

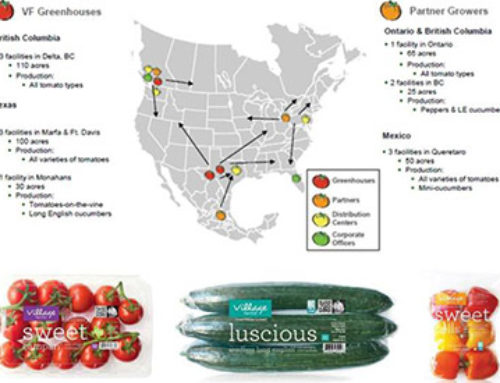

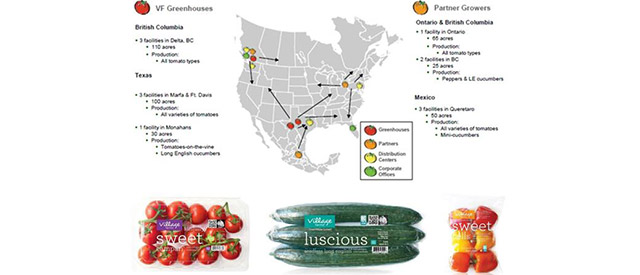

For those unfamiliar with the business, Village Farms has been operating for over 25 years and owns and operates 7 greenhouses covering 240 acres with distribution agreements covering an additional 146 acres. By recycling water numerous times through its irrigation system the Company’s tomatoes, for example, use 86% less water than field growers while yielding up to 30x the amount of output on the same amount of land. The Company has wider controls over the variables involved with the growing of plants – including light, water, carbon dioxide, air temperature, nutrients, and a variety of other factors. These systems are mainly soil-less and use hydroponic growing techniques to facilitate plant growth.

The Company’s reputation for high quality produce allows it to distribute its non-GMO tomatoes, peppers and cucumbers through major retail grocers that include: Walmart (NYSE:WMT), Safeway (NYSE:SWY), Sobeys, Sam’s Club, the Fresh Market (NASDAQ:TFM), Whole Foods (WFM), Publix (OTC:PUSH), BJs, Loblaws, Costco (NASDAQ:COST), Fred Meyer, Kroger (NYSE:KR), HEB, WinCo Foods, Trader Joe’s, Giant Eagle, Harris Teeter Supermarkets & Associated Wholesale Grocers.

The Company also developed a proprietary greenhouse technology known as Greenhouse Advanced Technology Expert System (GATES) for growing produce in extreme conditions; currently in use at the Monahans facility in Permian Basin, Texas, where outside temps can exceed 110 degrees Fahrenheit.

Financials Update – Looking Back at the April 2016 Report’s Projections

For 2016 and beyond, it’d been projected in the April 2016 Report for Village Farms revenue to increase because “the Company is at maximum acreage along with increased efficiency at Monahans via GATES, has a major distribution agreement with Great Northern that allows for sales in new markets and has the capabilities to support additional businesses such as berries or additional high margin crops.”

On May 10, 2016, in their quarterly earnings report issued one month after our report, Village Farms stated that Q1 2016 revenue and EBITDA grew 14% and 80%+, respectively, compared to the previous year and was due in part to “…continual yield improvement at our GATES technology greenhouse…Supply partner revenues also significantly increased by 34%.” The Company also went on to say that “These actions, coupled with the addition of some strong new team members, a new supply partner and new customers, gives us confidence in achieving our 2016 guidance of at least 15% year over year growth in both our revenues and EBITDA.”

This meant revenue for 2016 would be around $163 million USD and EBITDA around $11.7 million USD; in line with the projections from the April 2016 Report one month earlier, and other points raised, where it had been projected that ‘2016 revenue of $165 million and EBITDA approaching $12.5 million USD. Growth should continue into 2017 for revenues of $190 million and EBITDA of $15.5 million.’

Ultimately, revenues for 2016 increased 10% over 2015 to $156 million and EBITDA decreased 8% to $9.4 million; below expectations but due to industry-wide issues and not any Company-specific problems. Per the Company’s 2016 year-end filings:

The shortfall of (5%), or ($7.7M), against the previously issued guidance (for revenue) was due to a decrease in the selling price for the Company’s TOV and beefsteak varieties in 2016 versus 2015, a shortfall in the expected supply partner revenues related to lower than expected volumes and crop issues primarily relating to the TOV and beefsteak varieties at our Canadian facilities. The variation of ($2.3M) against the previously issued guidance (for EBITDA) was primarily due to a decrease in the selling price for the Company’s TOV and beefsteak varieties as compared to the year ended December 31, 2015. If average prices for TOV and beefsteak had been equal in 2016 to 2015 prices; EDITDA in 2016 would have increased by $3.5M.

The growth potential of Village Farms remains positive. The Company has started talking about building another GATES facility in the Southeast, similar to the successful operation in Texas. It has also been revisiting getting into the berries business – which represents the largest dollar contribution in retail produce. Village Farms appears focused on innovations in technology and distribution, as they have always been. Guidance for 2017 is maintained.

This brings us to last month’s announcement that Village Farms would be forming a JV with Emerald Health to pursue cannabis production and distribution. It had been alluded to a few times in the past, most recently being in the Company’s Q1 2017 filing where they stated ‘In addition to the Company’s continual focus on increasing its revenues and profits on core crops – tomatoes, cucumbers and peppers – the Company is actively exploring whether to produce certain higher margin alternative crops.’ Berries and cannabis production had previously been cited as potential target high margin crops. As of June 7th, cannabis appears to be the choice for the foreseeable future; one that could prove extremely profitable for Village Farms given their vast growing expertise, technology and capacity to convert many greenhouses for the JV.

Village Farms JV with Emerald Health Therapeutics

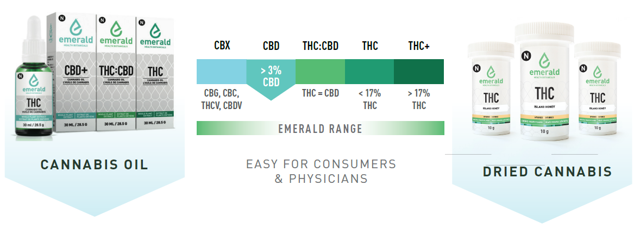

Emerald Health Therapeutics focuses on extraction and downstream product development; it grows unique strains of cannabis with the intention of treating medical conditions and developing consumer products. Emerald Health’s current product offering includes different types of cannabis oils and dried cannabis. The Company has a team of PhDs and MDs working to further develop a range of cannabis extraction-based products, while researching the effect of cannabis and cannabinoids on health in clinical studies. The combination of committed scientists and strains gives Emerald the ability to develop new varieties through plant genetics.

Emerald’s access to widely recognized experts in the development of botanical, nutraceutical and pharmaceutical medicines and the ability to carry out clinical trials could help them become a leader in the medicinal cannabis industry.

The JV allows Village Farms to pursue dual tracks by focusing on:

- Medicinal uses for a growing consumer market that the JV can market to directly, and

- The opportunity to be the experienced low-cost supplier in the Canadian wholesale market

The summary highlights from the JV announcement and the benefits it presents are as follows:

- Village Farms and Emerald Health, the 8th federal licensee under Canada’s ACMPR program, plan to be a low-cost producer and distributor of cannabis for medicinal and therapeutic purposes

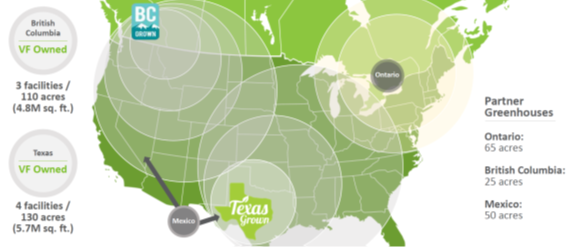

- Village Farms committed 1 of 3 Delta, British Columbia, Canada, greenhouses (25 acres or 1.1 million sq. ft.) for initial production that could yield 75,000 kg of cannabis annually; Emerald has committed C$20 million to fund conversion of the initial greenhouse

- The JV could access all neighboring greenhouses (110 acres or 4.8 million sq. ft. total) if mutually agreed for production, capable of yielding 300,000 kg of cannabis annually

- In Canada, where medicinal marijuana is legal and recreational legalization continues to gain traction, the total demand four years from now is estimated to be 600,000 kg annually

- Village Farms can supply half of the expected demand via conversion of existing facilities

- Currently the market’s capacity without the involvement of Village Farms is in total a mere 80,000 kg annually – this is spread between 37 companies with registered licenses

Capacity & Announced Future Capacity of Public Licenses with Market Cap > C$200 million

In a Cormack Report from April 2017, prior to the JV announcement, projections showed “installed capacity among nine of the larger LPs moving from ~60K kg/year exiting 2016 to over 350K kg/year by exit 2018 and over 500K kg/year by exit 2019. This capacity path compares to Cormark’s total market size estimate of ~600K kg/year (MMJ +RMJ) and still ignores the list of other existing LPs without public plans and new LPs likely on the way”.

No matter what level of additional capacity from competitors, Village Farms can be the largest producer in a market with strong demand. The Company has the additional advantage of needing only to convert existing facilities to meet market standards; competitors will need to invest significantly in new builds just to meet their projected capacity capabilities.

A prime example of successful conversions of greenhouses as planned by the JV is British Sugars’ swapping of its 45 acres of tomato plants for cannabis seedlings as part of a supply agreement with GW Pharmaceuticals (NASDAQ: GWPH). In 2010, GW created the world’s first prescription cannabis-derived drug in the form of multiple sclerosis treatment Sativex and soon it plans to launch Epidiolex, which has shown to be hugely effective in treating children with a deadly form of epilepsy. The Company uses the cannabis plants to produce Cannabidiol, CBD.

Tremendously impactful medicinal products could be produced from specially designed cannabis strains that are grown by the Village Farms/Emerald Health JV.

The Significant Positive Financial Impact of the JV

Focusing just on Canada and ignoring the even larger US market, the combination of the master growing expertise of Village Farms with the cannabis industry experience of Emerald Health Therapeutics could lead to major contributions to VF’s bottom line.

Village Farms has stated this could generate revenue 10-15x that of produce and with EBITDA margins greater than 50% based on a sub C$1.00/gram production cost; the industry average cost is C$2.25/gram. Village Farms has a clear advantage in being the leading low-cost producer.

On the revenue side, LPs are reporting average retail pricing of C$8 – C$10 per gram for medical marijuana and wholesale pricing of C$4 – C$5 for the recreational market.

Village Farms has a strong distribution network with strategically placed facilities. Cannabis growers would have to make considerable capital investments to increase their production capacities while Village Farms’ expenditures would only be focused on the conversion of existing facilities, as shown:

As further details become available on the economic details of the JV partnership, a more detailed analysis will be possible on the EBITDA impact of Village Farm’s cannabis production. For now, we will conservatively discount recent Company statements about production capacity (75,000 kg starting in 2019), full capacity capabilities (300,000 kg if all Canadian greenhouses are in use), likely EBITDA margins (above 50%) and market information about wholesale and retail prices (based on the Cormack Report).

To highlight the tremendous upside potential of EBITDA impact for Village Farms from the JV, profit estimates included below are extremely conservative. We show revenue starting in 2019, although Village Farms predicts cannabis revenue beginning in 2018. In addition, although the Company projects EBITDA margins over 50%, we show 40% with decreases over time due to increased competition. Lastly, while market reports show potential retail prices ranging from C$8 – C$10 per gram, and half that for wholesale, we use an average of C$5.50 for 2019 decreasing to C$4.50 in 2023.

Five-year EBITDA projections starting in 2019 are therefore as follows, and assume Village Farms participates in 50% of all of the JV’s profits:

*** It should be noted that total production capacity would be 300,000 kg if all three Canadian greenhouses were brought online at any time and 650,000 kg total should Village Farms ever decide the market opportunities in the United State warrant a full conversion of all US greenhouses as well.

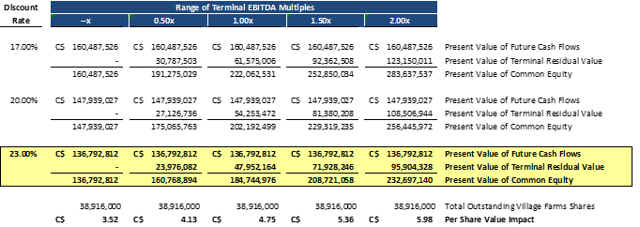

A discounted cash flow sensitivity analysis using these conservative EBITDA projections is then provided with increasing discount rates and low terminal EBITDA multiples. The per share value impact of C$4.13 to C$5.98 is based on a discount rate of 23% and terminal EBITDA multiples ranging from 0.5x to 2.0x, per the yellow highlighted section below:

With overly conservative scenarios for production capacity/usage, revenue ramp up, EBITDA margins, pricing of cannabis, discount rates and terminal EBITDA multiples, the price impact would still be a significant C$4 – C$6 per share or $3.30 – $4.75 USD per share. The reality could likely be far greater.

And if using transaction multiples (Canopy Growth Corp.’s purchase of Mettrum Health in January 2017 for 12.9x 2019E EBITDA) or average trading multiples (peer group from Echelon Report showing 12.8x 2019E EBITDA), Village Farms 2019E EBITDA JV share of C$44 million would imply additional share value of around C$14.50 or $11.50 USD. More recently, and conservatively, Cormack suggests 9x EBITDA – still C$10+ per share or almost $8 USD per share.

Given the JV upside potential, we think Emerald Health is a great stock to own as well.

Village Farms Remains Undervalued

Village Farms remains significantly undervalued. The Company is trading at 1.1x its book value, a slight improvement over the 0.7x at the time of our April 2016 report but still low given the 240 acres of top quality and technologically advanced acres that contribute to its profitability; even more so when considering the ability to expand into new markets such as Canadian cannabis. The Net Book Value of physical holdings based on the first quarter of 2017 is at $94.6 million; adjusting for the $45 million invested in the 30 acres at the Monahan facility, the per acre book value is around $0.235 per acre. Recent transactions include capital investments of $0.7 million to $2.7 million per acre for produce production by competitors; Village Farms’ 240 acres continue to be undervalued in comparison.

The Company’s core business of being a premier grower of produce remains intact and growing but their JV announcement is a promising development demonstrating the Company’s ability to utilize its production capabilities and technology prowess by entering higher margin industries. As we have shown, the potential profit implications are significant. Should cannabis demand in Canada continue to grow quickly, the Village Farms JV will be in a position to convert 110 acres to full production while Texas and partner acreages totaling another 270 acres continue their successful focus on the traditional produce market. If the regulatory market in the United States ever changes, Village Farms will also be in an excellent position to benefit even further should they want to do so.

Village Farms is a profitable greenhouse grower, with excellent produce distribution and technology that can be utilized in the harshest of climates. To further its profitability, the Company’s expansion into the Canadian Cannabis industry provides additional upside for an already undervalued and well-diversified hydroponic investment. No publicly traded companies in this sector can say the same. In an industry that is ripe for potential consolidation, Village Farms is a leading candidate to be a successful acquirer.

We think the Company should be trading above $2.50 USD in the near future and above $4.00 USD around the release of its 2017 annual report next year.

The market continues to undervalue its technology-superior acreage, revenue increases via numerous distribution agreements, expansion of GATES technology and now the promise of impactful margins from the Canadian Cannabis industry.

Disclosure:I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Disclaimer

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal, tax advice, or investment matters and readers are advised to consult their own professional advisers. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

First Bridge Investment Group does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Any discussion in this document of past or proposed outcomes should not be relied upon as any indication of future outcomes. First Bridge Investment Group does not have any duty to you, whether in contract, tort, under statute or otherwise with respect to or in connection with this publication or the information contained within it. To the fullest extent permitted by law, First Bridge Investment Group disclaims any responsibility to liability to for any loss or damage suffered or cost incurred by you or by any other person arising out of or in connection with you or any other person’s reliance on this publication or on the information contained within it and for any omissions or inaccuracies.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}