Summary

Since our April 2016 initiating report and our July 2017 follow‑up on Village Farms International (“Village Farms” or “VFF”), the company has transitioned from an overlooked hydroponic greenhouse operator into a vertically integrated participant in the Canadian cannabis market. Pure Sunfarms, the company’s 50%-owned cannabis joint venture, is now licensed across its full 1 million square foot Delta 3 facility, has begun commercial sales, and delivered positive net income for 2018.

Village Farms’ common shares have performed significantly well since our earlier articles, helped by Pure Sunfarms’ progress, the recent Nasdaq listing under ticker “VFF,” and the launch of a U.S. hemp/CBD strategy. At today’s valuation, we believe a substantial portion of our original upside thesis has been recognized by the market. The risk/reward profile is now much more balanced than it was in 2016–2017.

For long-time shareholders who have held through this entire period, we view the current environment as a reasonable opportunity to realize gains, either fully exiting or significantly reducing exposure.

Background: From Undervalued Greenhouse Operator To Cannabis Platform

In April 2016, our first Village Farms article introduced the company as a “rare undervalued equity investment opportunity in the AgTech sector.” At that time, there was no sell-side research coverage on the name. We were, to our knowledge, the first long-form public equity research on Village Farms, even though the company had operated for years as one of North America’s largest producers of greenhouse-grown tomatoes, peppers, and cucumbers.

That initiating report highlighted several key points:

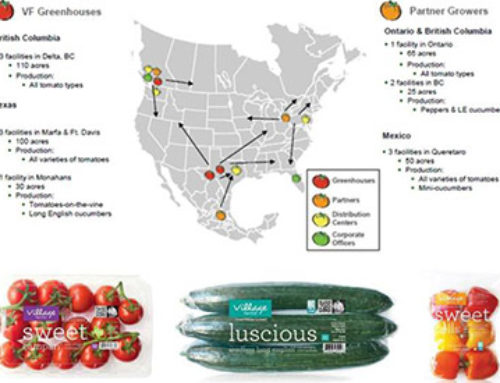

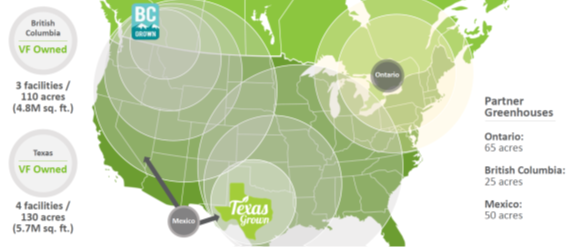

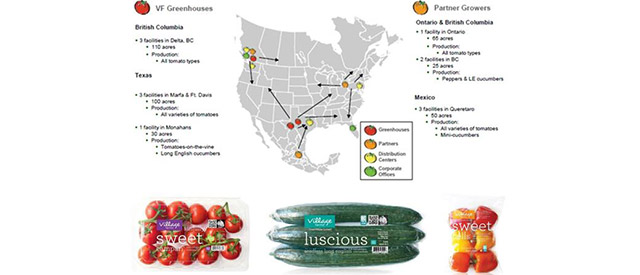

• Village Farms owned and operated 240+ acres of greenhouse capacity, with additional acreage accessed via distribution agreements, supplying major North American grocers.

• The company had developed proprietary GATES greenhouse technology, enabling high yields and materially lower water usage compared to field growers, an increasingly valuable attribute in a world of water scarcity and food safety concerns.

• Despite these strategic assets, the stock traded at a discount to the replacement value of its greenhouse footprint and at a modest multiple of normalized earnings, with limited investor attention.

Our July 20, 2017, follow‑up article focused on the newly announced Pure Sunfarms joint venture with Emerald Health, a 50/50 cannabis JV that would repurpose existing greenhouse capacity in Delta, British Columbia. That second report argued that:

• Village Farms’ greenhouse infrastructure, operational team, and retailer relationships provided a durable advantage in cultivating cannabis at scale.

• The JV structure offered a low-risk, high-optionality way for Village Farms to participate in the Canadian adult-use cannabis opportunity while preserving its core produce business.

• The public market was not yet appropriately valuing the potential earnings contribution from the Delta 3 conversion as the cannabis platform matured.

At that point, Village Farms still remained essentially uncovered by traditional equity research firms. Today, by contrast, the company is followed by multiple Canadian and U.S. analysts, underscoring how far the story has moved.

Developments Since Our July 2017 Cannabis Report

Pure Sunfarms’ progress over the last 18–20 months has moved much of the “option value” we highlighted in 2017 into the realm of realized economics.

Pure Sunfarms licensing and profitability

According to Village Farms’ fourth quarter and full-year 2018 results:

• Village Farms’ share of Pure Sunfarms’ net income in 2018 was US$2.4 million, including US$2.8 million in the fourth quarter alone.

• Pure Sunfarms generated positive net income in its first full quarter of sales and was profitable for the full year.

• Health Canada license amendments have allowed Pure Sunfarms to expand its licensed production area to the entire 1 million square foot Delta 3 greenhouse.

These facts validate core elements of our 2017 thesis: the Delta 3 asset could be converted efficiently for cannabis production, and Village Farms’ long experience with greenhouse operations translates into competitive performance in a new, higher-value crop.

Commercial channels and non-dilutive financing

Pure Sunfarms has also moved beyond “just production” into commercially relevant channels:

• It has been selected by the Ontario Cannabis Store, Canada’s largest provincial distributor, to supply branded products into the recreational market.

• It has entered into a wholesale arrangement with a major online medical cannabis platform, providing additional volume outlets and brand visibility.

• A CAD$20 million term loan with Bank of Montreal and Farm Credit Canada helps complete the Delta 3 conversion and supports general corporate purposes, providing non-dilutive growth capital for the JV.

Together, these steps reinforce that Pure Sunfarms is not merely a licensed facility, but an operating business with profitable production, distribution, and financing in place.

Capital markets upgrade: Nasdaq listing

Village Farms has also recently materially improved its capital markets profile. In February 2019, the company’s common shares began trading on the Nasdaq Capital Market under the symbol “VFF,” while continuing to trade on the Toronto Stock Exchange.

A U.S. national exchange listing typically broadens the eligible shareholder base (particularly among U.S. institutions and funds that cannot own OTC names), enhances liquidity, and can support a higher valuation multiple when fundamentals are perceived as solid. We believe this listing has been an important catalyst in the recent share price performance.

Emerging U.S. hemp/CBD optionality

The December 2018 U.S. Farm Bill legalized hemp cultivation and hemp-derived products at the federal level. Village Farms moved quickly to capitalize on this development:

• It formed a 65%-owned joint venture, Village Fields Hemp, with the Jennings Group to pursue outdoor hemp cultivation and CBD extraction in multiple U.S. states.

• Management has articulated an intent to build a vertically integrated hemp-derived CBD business, leveraging Village Farms’ existing relationships with large retailers and, over time, its greenhouse footprint in Texas as regulations allow.

While still currently in its early stages, this U.S. hemp/CBD strategy represents a second layer of optionality on top of Pure Sunfarms and stands in sharp contrast to the company’s situation when we first initiated coverage as an almost completely ignored greenhouse grower.

Share Price Performance And The Evolution Of Coverage

The share price performance of Village Farms over the past several years has been dramatic since we initiated coverage:

• A gain of more than 500% in 2017, driven by investor enthusiasm around the cannabis JV and the broader Canadian cannabis bull market.

• A sharp pullback in 2018, with the stock declining roughly 40–50% from its peak, as cannabis stocks corrected and the produce business faced margin pressure.

• A strong rebound in early 2019, with shares nearly doubling off the late-2018 lows, aided by Pure Sunfarms’ profitability, licensing progress, and the Nasdaq listing.

For readers who have followed our work since the April 2016 initiating report and the July 2017 cannabis update, this translates into a multi-bagger outcome from the $1.14/share (market cap of $44 million) at our first report and $1.53/share (market cap of $60 million) at our second report to current levels several times higher, even after periods of volatility.

Equally noteworthy is the evolution of research coverage around the name. When we published our first Village Farms report in 2016, there was no formal sell-side research, and the stock was effectively ignored by institutional investors. Now, multiple Canadian and U.S. firms publish research on Village Farms. We believe our early work helped frame the investment case for a business that was, at the time, almost entirely overlooked.

The contrast is clear: what began as a small-cap, under-followed greenhouse grower trading below the value of its assets has become a more widely followed operator with a meaningful institutional shareholder base.

Reassessing Risk And Reward At Current Levels

With the share price now reflecting much of the good news, we believe it is appropriate to revisit the risk/reward trade-off for new capital and for long-time shareholders.

The market has now broadly recognized

• The existence of Pure Sunfarms as a profitable, scaled producer of cannabis.

• Licensing of the full Delta 3 footprint, with the potential to generate significant production volumes.

• Early evidence that Village Farms’ greenhouse expertise translates into competitive economics in cannabis.

• Strengthened balance sheet support for the cannabis project via non-dilutive bank financing.

• The capital markets uplift associated with a Nasdaq listing and broader investor awareness.

What remains as upside optionality

The remaining upside now lies more squarely in execution and expansion. Key areas of residual upside include:

• Full utilization of the Delta 3 facility at targeted yield and cost metrics, and the potential for expanded capacity beyond Delta 3 over time.

• The possibility, depending on future decisions and JV dynamics, for Village Farms to increase its economic interest in Pure Sunfarms.

• Successful execution of the U.S. hemp/CBD strategy, including regulatory clarity in key states, the scaling of cultivation and extraction, and commercialization of branded or private-label products through large retail partners.

Key risks from here

Against this, we see several risks that are more consequential at today’s higher valuation:

• Cannabis wholesale pricing pressure as more licensed capacity comes online across Canada, potentially compressing margins for even efficient producers like Pure Sunfarms.

• Regulatory or execution challenges in both cannabis and hemp, including delays in permitting, testing, or product approvals.

• Persistent margin compression or volatility in the core produce business, which could continue to weigh on consolidated results.

• The possibility that investor sentiment toward cannabis broadly becomes more cyclical, leading to greater volatility in Village Farms’ share price than would be justified by fundamentals alone.

In 2016 and 2017, the asymmetry was heavily skewed in favor of the long side: a solid, asset-rich business with limited coverage and a free or nearly free option on cannabis. Now, the easy money has likely been made. The setup now appears more balanced, with both genuine long-term upside and a more meaningful set of risks to future returns.

Implications For Long-Term Shareholders

For investors who have held Village Farms since our initiating report in April 2016 or at least since our July 2017 article, the investment has, despite volatility, likely generated substantial gains.

We see three practical approaches for long-time shareholders:

Harvest and redeploy

For those whose original thesis centered on the market eventually recognizing the value of Village Farms’ assets and cannabis optionality, that outcome has largely occurred. From this vantage point, it is reasonable to treat Village Farms as a successful case study in value realization and to reallocate capital to the next mispriced opportunity where we can again be early rather than late in the discovery process.

Scale back, keep a residual position

A second approach would be to realize a majority of gains while maintaining a smaller position to participate in any further upside from Pure Sunfarms’ growth or the U.S. hemp/CBD strategy. This balances participation in long-term growth with a more conservative risk posture, recognizing that the valuation now embeds a substantial amount of optimism.

Remain fully invested, with adjusted expectations

More aggressive shareholders may choose to stay fully invested, viewing Village Farms as an evolving cannabis and hemp platform with a defensible produce base and unique greenhouse assets. For this camp, we would simply emphasize that forward returns are unlikely to resemble the past three years, and that position sizing and risk management become more important at current levels.

Our own inclination, leans toward the first two paths. For long-time shareholders, this is a rational window to exit profitably or at least substantially de-risk the position, while still recognizing Village Farms as a legitimate long-term platform in cannabis and hemp.

Final Thoughts

Village Farms’ journey over the last several years illustrates several broader points about public-market investing in under-followed names.

High-quality, asset-backed businesses can remain undervalued for extended periods until a visible catalyst, in this case, cannabis and hemp, forces investors to revisit the narrative. Deep operational expertise and existing infrastructure can be reused to participate in adjacent growth markets, often at a fraction of the cost and risk of greenfield entrants. When the market finally embraces a story, the valuation can move quickly from “cheap” to “fully valued or higher,” particularly in sectors that attract momentum and retail enthusiasm.

From our standpoint, Village Farms has largely executed on the strategy we outlined in 2016 and 2017: leveraging its greenhouse platform to participate in high-growth categories while maintaining its core produce franchise. The recent financial results, Pure Sunfarms’ profitability, and the Nasdaq listing collectively validate that effort. The flip side of that success is that the simple, deeply contrarian angle that originally attracted us is no longer present.

We also note with some satisfaction that when we first wrote about Village Farms in 2016, there was no formal research coverage, and very few investors were paying attention. Today (as of March 15, 2019) the company is followed by multiple analysts and a growing base of institutional shareholders. That shift in attention and understanding is exactly what long-term, research-driven investing seeks to capture.

For investors who joined the story early, we believe today’s environment represents a sensible moment to acknowledge that the core thesis has largely played out, and to consider locking in what has become a very profitable outcome.

Disclaimer

This article is for informational purposes only and reflects our views as of March 15, 2019, based on publicly available information. Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal, tax advice, or investment matters and readers are advised to consult their own professional advisers. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

First Bridge Investment Group does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Any discussion in this document of past or proposed outcomes should not be relied upon as any indication of future outcomes. First Bridge Investment Group does not have any duty to you, whether in contract, tort, under statute or otherwise with respect to or in connection with this publication or the information contained within it. To the fullest extent permitted by law, First Bridge Investment Group disclaims any responsibility to liability to for any loss or damage suffered or cost incurred by you or by any other person arising out of or in connection with you or any other person’s reliance on this publication or on the information contained within it and for any omissions or inaccuracies.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}