Summary

Village Farms appears to be a greatly undervalued stock in the Agricultural Technology sector.

Indoor Farming is a particularly attractive area where there are limited public investment opportunities.

The demand for investment opportunities in the Agriculture Technology sector continues to grow.

Based on their capital allocations, investors seem to be in agreement with projections of global food shortages to come from rising populations, scarcity of arable land and untenable demand for what is “poised to be the commodity of the 21st century“, water. AgTech investments will provide high returns given the solutions that these innovative businesses can provide.

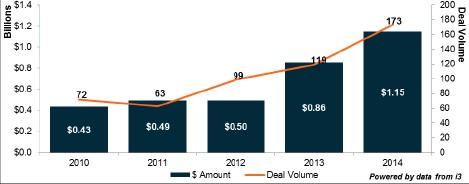

Private investment specifically in AgTech (agricultural technology) was relatively flat before 2013. Most tech innovation in agriculture was narrowly concentrated in biotechnology and seed genetics, and both investment and innovation were limited to players with close ties to the agriculture sector. Outside of seed genetics and crop inputs, most other AgTech was typically bundled with Cleantech. Then, in 2013, there was a shift. AgTech grew 75 percent to reach $860 million across 119 deals. The largest deal in the AgTech sector for 2014 came from KKR’s (NYSE:KKR) $90 million investment into Sundrop Farms, a company working to integrate solar-powered desalination technology with efficient greenhouses capable of growing food in the most arid climates. Indoor cultivation systems received an unprecedented amount of funding in 2014 and the vast majority of investment was focused on US-based companies.

In North America particularly, the demand for investment in this sector continues to grow. In February, Avrio Capital, a Canadian AgTech late-stage venture capital firm, closed its third food and agriculture technology fund on $110 million. It joined Seed 2 Growth Ventures’ $125 million Fund I and Cultivian Sandbox’s $115 million Fund II in a sector that has gained visibility as a viable venture asset class.

“The adoption of technology along the agricultural value chain is occurring at an unprecedented pace. Food security, wellness, sustainability and the digitization of the farm are just a few of the macro themes creating a new class of ag-tech companies that are redefining the ways in which we feed the world.”

Annual Global Venture Investment in Agriculture & Food Technologies

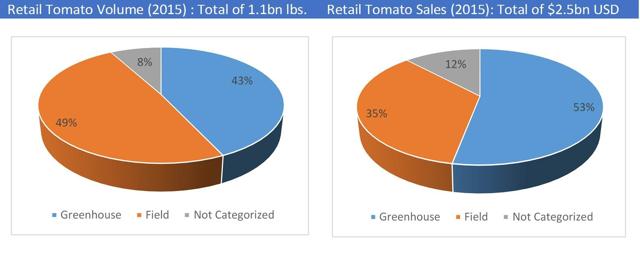

The 2014 US market for fresh vegetables was estimated at $25.2 billion, with a forecast annual growth rate of 1.2% to 2019. More than 1/3 of this value is estimated to be in crops that could be grown indoors – a $9.3 billion market. Greenhouse and vertical farm sectors are experiencing faster growth, and diets continue to trend in favor of sustainable, non-GMO producers. The food service industry and ongoing penetration of the retail grocery market provide ample opportunities for increasing revenue.

There are currently over 250 greenhouse vegetable companies. Canada has ~3,300 acres of greenhouses while the U.S. has ~1,300 acres. Of all the notable players in the indoor tech industry below, there’s only one real opportunity to invest in the growing hydroponic sector, Village Farms(OTCQX:VFFIF) and (TSE:VFF).

Two things should stand out from the competitive landscape. One, the majority of the companies in this sector are private, with only two companies providing a clear opportunity to invest in hydroponically grown produce. Two, Terra Tech (OTCQX:TRTC) (trading at 22.8x book value) appears overvalued while Village Farms (trading at 0.7x book value) appears greatly undervalued given their valuations and production capacities.

| Company | Description | Facilities Owned |

| Selection of Private Companies | ||

| Houweling | Mainly tomatoes, some cucumbers. | 125 acres in Camarillo, CA 50 acres in Delta B.C. 28 acres in Utah |

| Mastronardi | Non-GMO tomatoes, peppers and cucumbers. SUNSET brand and distribution of private label. |

189 acres; 63 acres in Quebec via 49% ownership agreement |

| Windset | Mainly tomatoes, peppers, cucumbers & lettuce. Landec (NASDAQ:LNDC) owns ~27% of the Company – allocates a FMV of $62.5 million USD on its position, which implies a Windset value of ~$230 million USD |

128 acres in Santa Maria, CA; 80 additional acres in Las Vegas, NV and Delta, B.C. Markets 540 additional acres for other greenhouse operators |

| Great Northern | Produces 26 million pounds of tomatoes annually. Signed distribution deal with Village Farms in May of 2015. | 65 acres in Ontario. |

| Red Sun Farms | Non-GMO tomatoes, peppers, cucumbers, eggplants. “97% of production exported to the US/Canada through the Pharr, Texas, distribution center.” | 250 acres in Mexico. 233 acres in Ontario. 18 acres in Virginia. |

| NatureSweet | Acquired EuroFresh and its 318 acres of greenhouses in April 2013 out of Chapter 11. Primarily grows tomatoes. | 9 facilities in the US & Mexico; ~400 acres USA, 1,100+ Mexico |

| Bright Farms | Builds greenhouses at or near urban groceries.

Raised a Series B of $14M on 11.6.15 |

Long-form purchase agreements for multiple builds. |

| Aero Farms | Vertical farming. Leafy greens. White-label produce. Raised a Series B of $20M on 12.10.15 |

2.4 acres just came online |

| Selection of Publicly Traded Companies | ||

| SunSelect | Primarily bell peppers and tomatoes. Distribution via the Oppy Group, a division of Total Produce (Ireland/England) | 100 Acres in Southern California and B.C., Canada |

| Terra Tech | Hydroponic greenhouse grown produce & cannabis.

Market Cap: $143.5M Book Value of Equity: $6.3M |

6 acres in Indiana/Nevada. 5 acres in New Jersey. |

| Village Farms | Hydroponic greenhouse grown tomatoes, peppers, and cucumbers. Distribution primarily in the US and Canada.

Market Cap: $44.1M Book Value of Equity: $62.9M |

240 acres owned & additional 130 acres in distribution partnerships with producers. |

A deep-dive analysis of Village Farms International continues below.

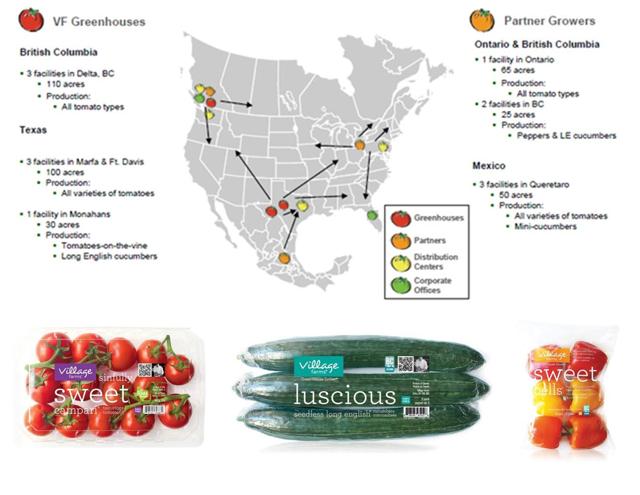

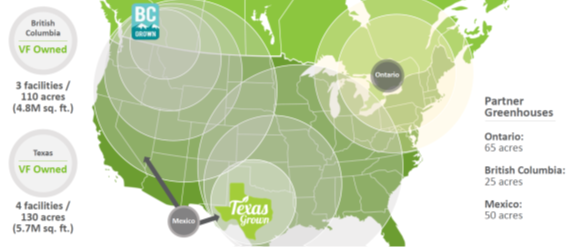

Village Farms (VF) stands out as a unique opportunity to invest in an undervalued hydroponic grower in the AgTech sector with the expertise, size and technology to supply produce in a sustainable and resource efficient manner. The Company has been in business for over 25 years and now owns and operates seven greenhouses covering 240 acres with distribution agreements covering an additional 146 acres. By recycling water numerous times through its irrigation system, the Company’s tomatoes use 86% less water than field growers while yielding up to 30x the amount of output on the same amount of land. The Company has wider controls over the variables involved with the growing of plants – including light, water, carbon dioxide, air temperature, nutrients, and a variety of other factors. These systems are predominantly soil-less and use hydroponic growing techniques to facilitate plant growth.

Village Farms maintains some of the highest food safety scores in the industry. The Company’s reputation for high-quality produce allows it to distribute its non-GMO tomatoes, peppers and cucumbers through major retail grocers that include: Wal-Mart (NYSE:WMT), Safeway (NYSE:SWY), Sobeys, Sam’s Club, the Fresh Market (NASDAQ:TFM), Whole Foods (WFM), Publix (OTC:PUSH), Target (NYSE:TGT), BJ’s, Loblaw (OTCPK:LBLCF), Costco (NASDAQ:COST), Fred Meyer, Market Basket, Kroger (NYSE:KR), HEB, Albertsons (NYSE:ABS), WinCo Foods and Associated Wholesale Grocers.

Looking ahead for this year, the Company should see an increase in capacity and revenue in 2016 from a distribution agreement with Northern Hydroponics that was signed in May. Northern Hydroponics is one the region’s most well-known greenhouse growers and owns 65 acres in the premier Leamington area.

The Company’s products are in line with consumer trends and the eating habits of developed economies like Canada and the US that continue to seek out a sustainable, resource-efficient approach to provide high-quality produce. Village Farms provides “local produce” to its retail customers from “farm to table in about three days or less.” Growing indoors in soil-less systems inherently limits exposure to many soil-borne pathogens that may have caused E. coli or salmonella. The safety standards and ability to trace produce through the supply chain are also hard for field growers to replicate, especially smaller suppliers. Such features should lead to continued growth in the retail produce market and penetration of the food service industry, where companies like Chipotle (CMG) provide examples of field grown problems. Expect food service providers to look to hydroponically grown produce like the retail grocery market has done.

Source: Village Farms – excludes Costco and BJ’s which are 100% Greenhouse retailers.

Proprietary Technology

The Company developed a proprietary greenhouse technology known as Greenhouse Advanced Technology Expert System (GATES) for growing produce in extreme conditions. At its Permian Basin Facility in Monahans, Texas, the Company is growing in an area where temperatures can get as high as 117 degrees F in the summer while winter months bring snow and harsh rains. This semi-closed greenhouse is a part of the strategy to build facilities that can produce quality hydroponic produce in harsh conditions.

“Village Farms made a $45 million investment in the Monahans Permian Basin facility,” said the Company’s CEO and Co-Founder, Michael DeGiglio, “and it’s continuing on this strategy platform into the future. This first commercial ‘Gates’ facility is 30 acres, and is also where the ‘Gates’ research center is located.” The company is continuing its research to advance its technology for use in future years and in many areas – even possibly extending to offshore countries. “Gates” technology’s more enclosed atmosphere enables Village Farms to better control the airflow and climate. It maximizes beneficial insect populations through the use of integrated pest management, IPM; a far more sustainable alternative to the use of chemical pesticides. It also enables the company to produce hydroponically in more severe climates. In the future, such technological developments for increasing yields in even the harshest environments could be licensed to other growing facilities.

Financial Information

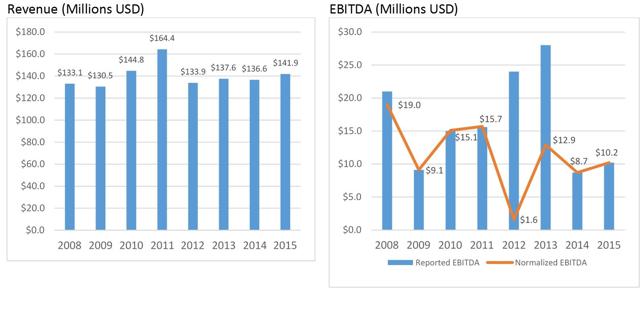

On May 28, 2012, the Company’s 82-acre facility in Marfa, Texas, saw greenhouses partially or completely destroyed by a “once in a hundred years” hail storm. After a record year of profitability in 2011, the Company’s production capabilities took a hit due to the storm just as its Monahans facility was coming online. By the end of June in 2014, the Company was harvesting 60 of the 82 acres that had been destroyed – 20 acres continue to be on hold.

A timeline of total acres in production may be helpful in reviewing historical revenues and projecting 2016:

2015 was the first full year for VF back at close to pre-hail capabilities with the added technological efficiencies (GATES) that have since been incorporated at the Monahans facility. The Company has also continued to increase its own production of exclusive varieties like its Mini San Marzanos, as well as expand the production of these exclusive varieties with its supply partners. As a result of the outlook for such exclusive varieties, the Company was able to enter into a new distribution agreement with Kingsville, Ontario, grower Great Northern Hydroponics, a subsidiary of Detroit-based, Soave Enterprises. The effect should be extremely positive for 2016 as the benefits to earnings can already be seen in the recent 2015 annual filings. Great Northern will ramp up from 15 acres of winter production to 60+ acres in April – the increased capacity should have a significant effect on revenue and EBITDA.

Village Farms is Significantly Undervalued

In reviewing the Company’s balance sheet, you will find two significant highlights:

1) The discrepancy between the Company’s book value and market value of equity

2) The apparently low book value attributed to the 240 acres of greenhouse the company owns

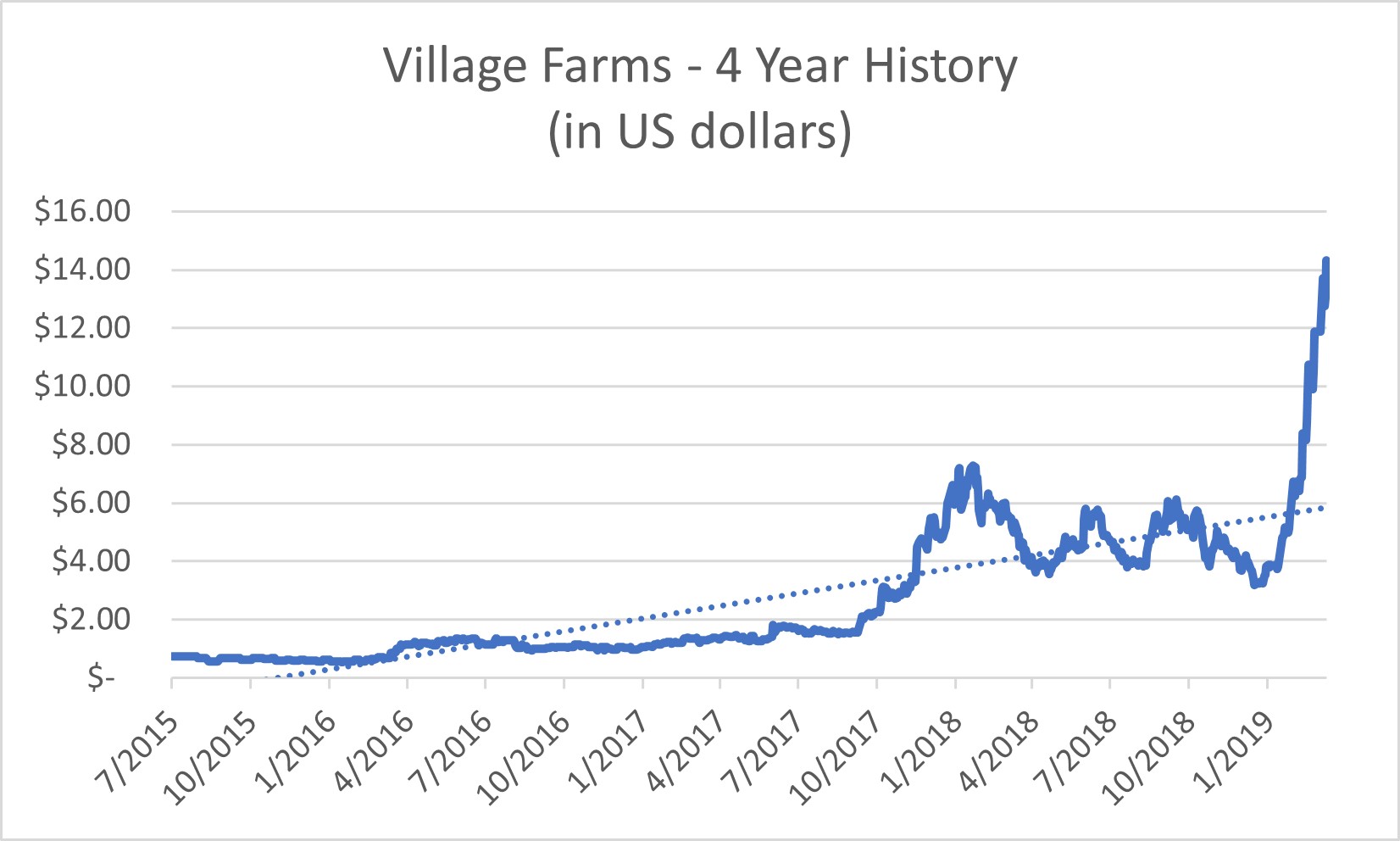

Undervalued Share Price

Over the past nine months, Village Farms had been trading at $0.60-0.70 USD per share with a market capitalization of $23.3-27.2 million USD based on 38.807 million shares outstanding.

On March 16, 2016, Mastronardi Investment Holdings purchased approximately 20% of outstanding shares at $0.96 USD per share, a 33% premium to the trading price; along with a positive earnings release for 2015 distributed at the end of last month, the stock is now trading at $1.14 USD per share as of April 4, 2016.

Book value on equity is $62.931 million USD, implying a book value share price of $1.62 USD. Village Farms is currently trading at just 0.7x its book value.

Low Book Value for Greenhouse Acreage

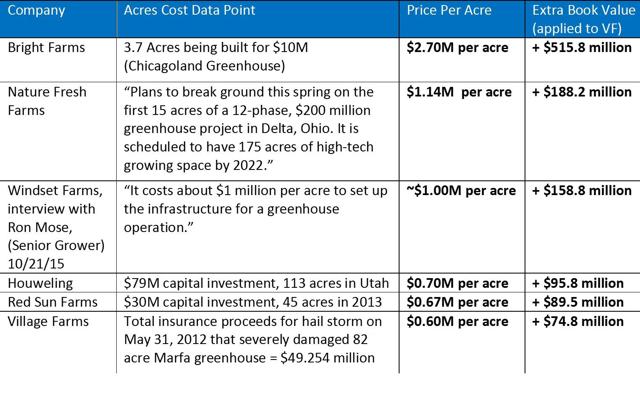

As of Q4 2015, the net book value for physical holdings is $94.285 million. For Village Farms’ 240 acres of greenhouses, this implies a book value of $0.393 million per acre. Considering that the 30-acre Monahans facility reportedly involved an investment of $45 million, the remaining adjusted per acre book value would be $0.235 million. This number seems to severely undervalue the holdings when comparing it to industry data points pertaining to the costs of greenhouse acreage.

Even a slightly higher per acre value would support significant value corrections as outlined below:

Validation of Potential Growth Plans Based on Significant Additions to the Team

The Company is led and was founded by Michael DeGiglio, a 30-year veteran of the industry with deep agricultural experience in controlled environment growing. The CFO of the Company, Stephen Ruffini, joined over seven years ago in 2009 and has over two and a half decades of experience in finance, operations, investor relations and M&A. Doug Kling, Chief Marketing Officer, and Bret Wiley, SVP of Sales, both have over 30 years of extensive sales, retail and marketing experience. It’s a strong management team at a company that is known as a leader in the industry with sought-after innovations in growing produce; experienced growers have allowed Village Farms to successfully enter new regions.

January 4, 2016: Dr. Roberta Cook accepted a position on the board of directors of Village Farms. Dr. Cook is a Cooperative Marketing Strategist at the Department of Agricultural & Resource Economics at UC Davis. She is a respected agricultural economist with extensive industry, market and trade knowledge. In response to her board appointment she commented that “Greenhouse vegetables are on target with consumer trends and are gaining a higher share of the ‘consumer stomach.'”

November 2, 2015: The Company created a new role, Director of Strategic Business & Sales Development, for Lyra Vance, a 14-year industry veteran with positions at The Oppenheimer Group (Oppy) and Transfresh Corporation. Oppy delivers over 100 varieties of produce from more than 25 countries – in North America, Oppy is particularly focused on greenhouse produce and berries. Transfresh, is interestingly an expert in “ensuring the quality and marketability of fresh berry products.”

It should be noted that berries represent the largest dollar contribution in retail produce and that the CEO of Village Farms mentioned during the Q3 2015 earnings call that Village Farms may eventually expand into the berry market, a high-growth and high-value segment.

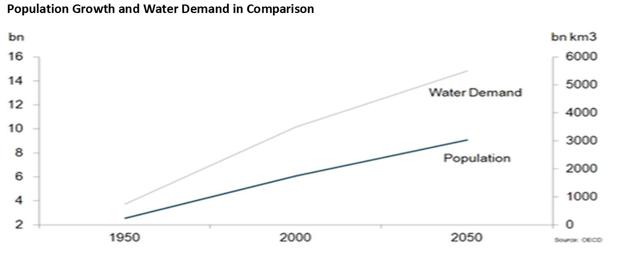

Significant increases in population growth combined with a decreasing amount of clean water and available land is leading to predictions of a global food crisis that would have far reaching effects. For most, technological advances in food production will be the only way to meet the unsustainable projected increase in food demand.

Food and agribusiness have a massive economic, social, and environmental footprint – the $5 trillion industry represents 10 percent of global consumer spending, 40 percent of employment, and 30 percent of greenhouse gas emissions (a 75% increase since 1990). Although sizable productivity improvements over the past 50 years have enabled an abundant food supply in many parts of the world, feeding the global population has reemerged as a critical issue.

If current trends continue, by 2050, the world will need to feed more than nine billion people, meaning that food production will need to increase by 70 percent, and crop demand for human consumption and animal feed will increase by at least 100 percent. At the same time, more resource constraints will emerge: 40 percent of water demand in 2030 is unlikely to be met and already, more than 20 percent of arable land is degraded – just 3% of the Earth’s total surface is arable land.

Depletion of natural resources, the impact of climate volatility on crops, and declining productivity gains in agriculture are expected to hinder growth in the world food supply, forcing countries to produce more with less. The pressure on water, land, energy, and labor resources will necessitate innovation to enhance agriculture productivity.

“The choice is clear,” says Hans Herren, World Food Prize laureate and the director of Biovision, a Swiss nonprofit.

“We need a farming system that is much more mindful of the landscape and ecological resources. We need to change the paradigm of the green revolution. Heavy-input agriculture has no future-we need something different.”

There are ways to deter pests and increase yields, he thinks, that are more suitable for the farmers of this world. Yes, indeed there is, perhaps none better suited to meet such important changes than hydroponic greenhouse farming. Village Farms is an undeniable value investment.

Aligned with Market Trends

– The projected disparity in resources to meet food and water demand in the near future requires agricultural tech (AgTech) solutions; with limited opportunities for investment in companies hydroponically growing food, VF provides a rare opportunity in this sought-after segment.

– Hydroponically grown non-GMO food is increasingly preferred by consumers; retail grocery market share will continue to rise and the food service industry holds major growth potential.

– Village Farms is a well-managed vertically-integrated operation that stands out in an industry that could start consolidating; reinforced by market signals from within the industry such as board additions (Dr. Roberta Cook, one of the industry’s foremost experts), new manager migrations (Lyra Vance from Oppy) and exclusive distribution agreements (Great Northern considered a premier Leamington area grower and previously with Mastronardi).

Acknowledgment from Market Experts of the Existing Value Opportunity

– On March 16, 2016, Mastronardi Holdings announced that it was purchasing approximately 20% of outstanding shares at $1.25 CAD/$0.96 USD; a 33% premium to Village Farms’ existing share price. Mastronardi’s purchase for “investment purposes” supports the undervalued analysis.

Increasing Revenue and a Target Share Price that Properly Values the Business

– For the next nine months of 2016 and looking ahead to 2017 and 2018, the Company is at maximum acreage along with increased efficiency at Monahans via GATES, has a major distribution agreement with Great Northern that allows for sales in new markets and has the capabilities to support additional businesses such as berries or additional high-margin crops.

– Based on the recently released annual figures for 2015 that saw revenue rise to $141.9 million and EBITDA increase by 18%, revenue for 2016 is projected to be $165 million with EBITDA approaching $12.5 million USD. This 16% growth in revenue assumes continued profit contributions from Great North distribution, as was seen to start materializing in the fourth quarter of 2015 per the latest filings. Growth should continue into 2017 for revenues of $190 million and EBITDA of $15.5 million.

– In line with its continued growth potential and market-leading operations, Village Farms should be trading close to $3.50 in two years as it releases its 2017 Annual Report. Along with an increase in earnings per share this takes into account an increased per acre book value compared to the current undervalued adjusted acreage rate of $0.235 per acre.

Supporting Documents

Disclosure:I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Disclaimer

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal, tax advice, or investment matters and readers are advised to consult their own professional advisers. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

First Bridge Investment Group does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Any discussion in this document of past or proposed outcomes should not be relied upon as any indication of future outcomes. First Bridge Investment Group does not have any duty to you, whether in contract, tort, under statute or otherwise with respect to or in connection with this publication or the information contained within it. To the fullest extent permitted by law, First Bridge Investment Group disclaims any responsibility to liability to for any loss or damage suffered or cost incurred by you or by any other person arising out of or in connection with you or any other person’s reliance on this publication or on the information contained within it and for any omissions or inaccuracies.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}