Summary

- Tornado Global Hydrovacs Ltd. is an undervalued leader in the hydrovacs industry, where innovative trucks are used for safe digging in areas with critical underground infrastructure (gas, telecom, water).

- Close to half a trillion dollars in proposed U.S. infrastructure spending is focused on work that’ll require the type of safe excavating that the hydrovacs industry is uniquely focused on.

- Newly opened 68,500 square foot facility in Red Deer, Alberta, triples Tornado’s hydrovac manufacturing capacity from 80 units to 240 units annually in an owned facility, eliminating outsourcing entirely.

- Tornado recently hired President Brett Newton, a hydrovac industry leader and co-founding partner of Rival Hydrovac, which sold 500 hydrovacs into the municipal market in the past five years.

- EBITDA will exceed $8 million in 2022 and reach $15 million by 2023. Share value should approach $1.50 per share as the ability to deliver 240 hydrovacs annually takes shape.

Introduction

On the heels of the Biden Administration’s “American Jobs Plan” and bipartisan negotiations, industries and companies that would benefit from such a major infrastructure initiative are receiving increased attention. Close to half a trillion dollars is focused on work that will require the type of safe excavating that the hydrovacs industry is uniquely focused on.

Executive Summary

An undervalued equity opportunity: Tornado Global Hydrovacs Ltd. (OTC:TRRNF) [TSXV:TGH]

- Newly opened 68,500 square foot facility in Red Deer, Alberta, triples Tornado’s hydrovac manufacturing capacity from 80 units in a former leased facility to now 240 units annually in an owned facility, eliminating outsourcing entirely. New plant is outsourcing all fabrication including paint and welding which will allow increased assembly times and quality control. Could diversify product lines via volumetric mixer or other equipment lines that complement hydrovacs.

- Well-located facility creates a major parts & services hub with 35-40% EBITDA margins.

- Large U.S. Tornado distributor merged with leading specialty distributor to utilities, doubling North American locations and increasing the reach of Tornado’s product offerings. (Working with U.S. dealer to improve distribution as well as customer experience which will increase sales. Current U.S. distributor is only targeting the Mid-West which is a quarter of the market. Reached an agreement with the Ontario East dealer to set up bricks and mortar sales and service in the GTA which is one of the largest markets in North America. Ontario dealer is also in the process of setting up bricks and mortar in Quebec. Assembling Tornado sales team that will support dealers as well as seek new opportunities.)

- Introduction of the F2 Tempest line (7 yards3 debris, 800 gallons water capacity), an environmentally conscious solution for the high-growth city/utility market (currently working with engineering to make unit as utility and municipal friendly, adding new features not seen on competitors’ vac trucks today.)

- Tornado insiders aligned with shareholders, particularly the largest insider, James Chui, who controls 41% of outstanding shares and purchased at an average price of $0.20 per share.

- Experienced management team led by CEO Bill Rollins and Non-Executive Chairman Guy Nelson. Tornado recently announced the hiring of President and COO Brett Newton, a hydrovac industry leader and co-founding partner of Rival Hydrovac (“Rival”), a competitor to Tornado that sold ~500 hydrovacs into the municipal market in the past five years.

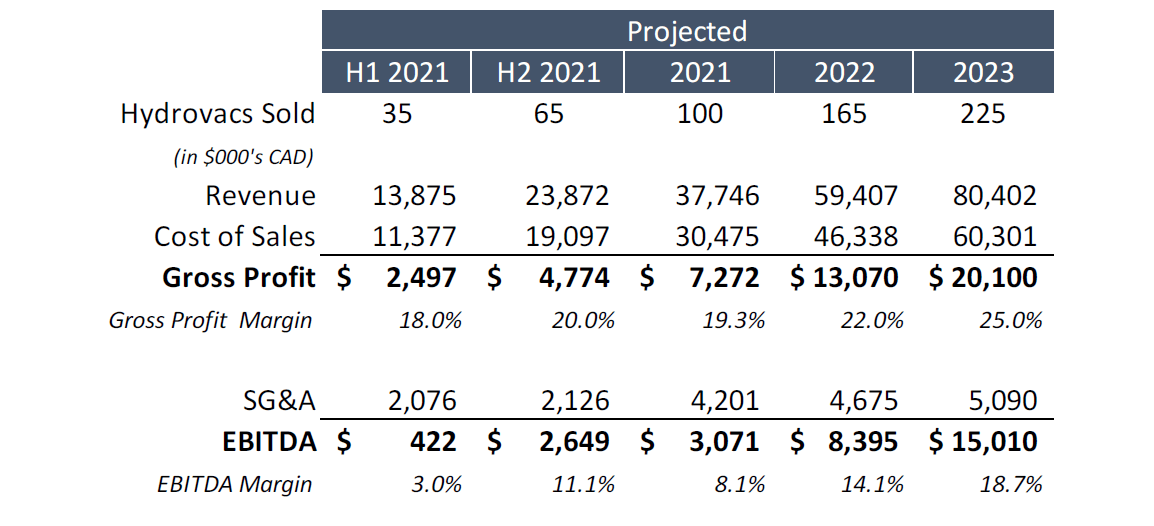

- Based on our projections, EBITDA will exceed $8 million in 2022 and reach $15 million by 2023.

- Even with conservative EBITDA estimates, it’s reasonable for share value to approach $1.50 per share as the ability to deliver 240 hydrovacs annually takes shape with support from the growing and recurring profits of the parts and services business.

“American Jobs Plan” Of the $579 billion in new infrastructure spending that is being proposed by the Biden Administration and bipartisan negotiations, these are the initiatives that have been detailed and would require the type of safe excavating that the hydrovacs industry is uniquely focused on.

- $109 billion: Modernize 20,000 miles of highways, roads, and main streets along with 10,000 small bridges and 10 of the nation’s most “economically significant” bridges.

- $73 billion: Power grid improvements.

- $65 billion: Put hundreds of thousands of people to work laying thousands of miles of transmission lines for affordable, reliable, high-speed broadband to all Americans, including the more than 35 percent of rural Americans who lack broadband at minimally acceptable speeds.

- $55 billion: Upgrade aging water systems (small water, household well and wastewater systems) and eliminate all lead pipes and service lines in our drinking water systems (six to ten million homes still receive drinking water through lead pipes and service lines).

- $47 billion: Weatherproofing, upgrades to coastal infrastructure, severe weather mitigation.

- $21 billion: Environmental projects.

- $16 billion: Cap hundreds of thousands of orphan oil and gas wells and abandoned mines.

Total: $386 billion

The Common Ground Alliance (CGA) and their Data Reporting & Evaluation Committee publishes the only comprehensive accounting and analysis of damages to buried infrastructure in the U.S. and Canada. Six months ago, they released the DIRT Report for 2019, which estimated $30 billion in societal costs in 2019 due to failures to prevent damages in the U.S. alone. Their reporting system also found the root cause of almost 30% of reported damages to be “excavation practices”, often when holes are dug with hand tools and backhoes; striking buried lines and causing a spill or breaking a cable, costly mistakes.

Hydrovacs Industry Overview

The industry has continued to grow throughout Canada and the United States because of the tremendous efficiency and safety it brings to daylighting, soil trenching, piling hole excavation, debris removal and cold-weather digging.

While initially tailored to the oil and gas sector, the hydrovac industry has rapidly expanded into the utility market where damages are common and more efficient solutions are in demand as well.

Estimates are that 1,500 hydrovac trucks are manufactured in North America annually. Key manufacturers include:

Image Source: Company Logos

Manufacturers sell direct and through distributors such as Camex Equipment, Custom Truck One Source (NYSE:CTOS), Transwest Truck and Trailer, JD Brule, and Ditch Witch (subsidiary of The Toro Company (NYSE:TTC)). Contractors, municipalities, and rental groups are the buyers. Large scale operators, most of which purchase from the highlighted manufacturers, include:

Image Source: Company Logos

The largest company in the industry is Badger Infrastructure Solutions Ltd. (OTCPK:BADFF), manufacturing its own trucks for exclusive use and operating a fleet of about 1,200 hydrovacs throughout North America. In 2020, Badger had CAD446 million of revenue in the United States with 962 hydrovacs and CAD113 million of revenue in Canada with 232 hydrovacs (166 of which are operated via franchise agreements).

In what Badger labels “core” and “strategic” markets, where there is a 50-500 and 500-1,500 truck market potential per location, respectively, the company estimates total hydrovac truck count growth potentials of ~5x and ~15x, respectively. In anticipation of such tremendous market potential, Badger intends to significantly increase its manufacturing to add an additional 600 hydrovac trucks to its fleet by the end of 2024. Badger trades at 2.8x 2020 Revenue and 15.7x 2020 EBITDA.

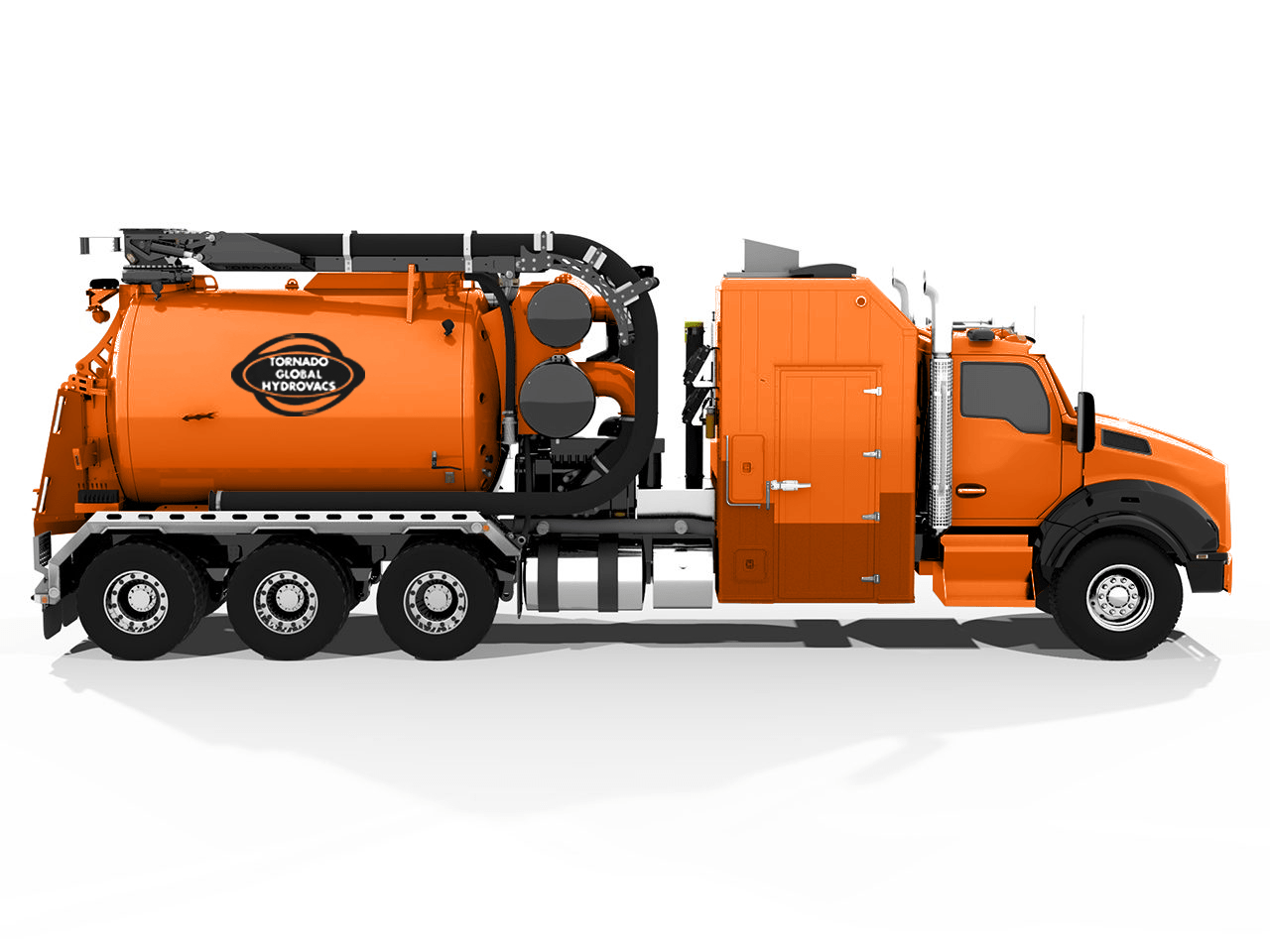

An Undervalued Equity Opportunity

Image Source: Company

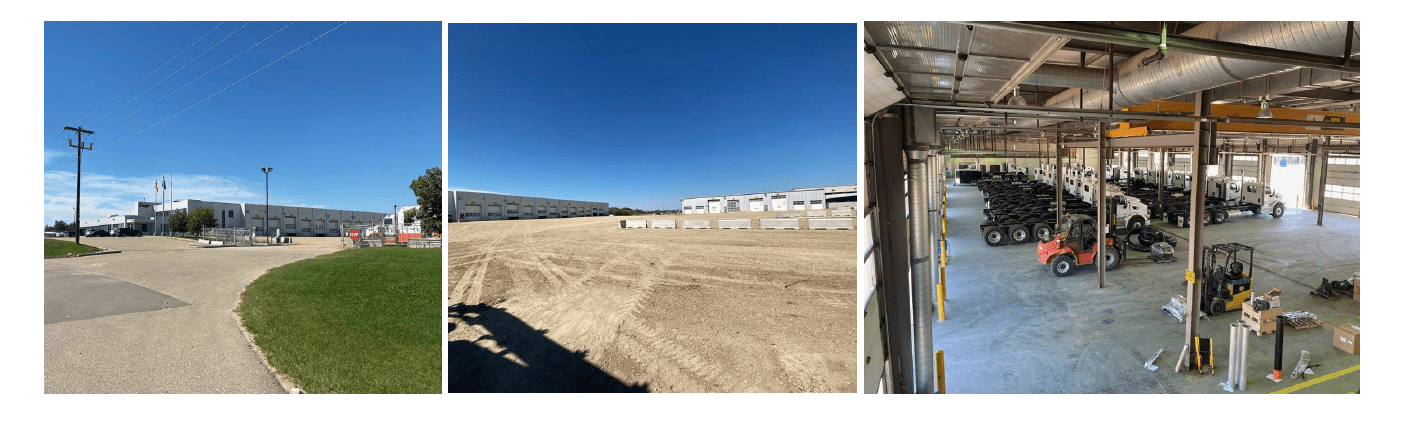

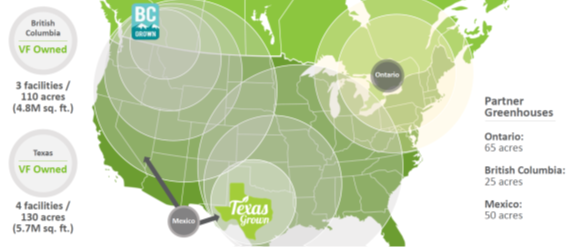

Red Deer Manufacturing Capacity Expansion

Prior to the Covid-19 pandemic, Tornado was selling 120 hydrovacs annually, 1/3 of which were outsourced and 2/3 produced in a leased facility operating at full capacity. Demand exceeded its manufacturing capacity so on February 3, 2020, the company purchased a 68,500 square foot facility built on 16 acres of land located in Red Deer, Alberta for $6.5 million. That facility will be operational this summer and allow the company to meet increasing capacity needs without any restrictions. The company will be able to manufacture up to 20 trucks per month (240/year), all from this new facility.

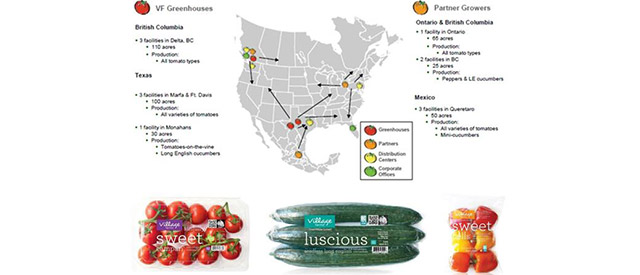

Growth of Tornado’s Parts and Service Business

In 2020, operating out of the leased facility it has now vacated, the company had a $4 million revenue contribution from its parts and services business (ten employees), the highest annual sales on record. In August of 2020, the Red Deer facility started being utilized for this growth under the direction of John Lavoie, an experienced operations manager previously at Clean Harbors. Management estimates that staff could grow 3x-4x in the next three years at this location.

With a team of licensed mechanics (Red Seal, Journeymen), a new 30’x100′ foot parts warehouse and five 110-foot bays, Tornado is in an excellent position to build a major inspection, repair and parts business servicing the Red Deer, Alberta, region. They can focus on medium and heavy-duty vehicles, not only hydrovacs, including major chassis manufacturers that can provide large volumes in parts and service business. Tornado, with its buying power, now becomes a major player in this market. In the new, much larger facility it owns, sales of parts and service are expected to significantly increase in 2021.

Image Source: Company, www.tornadotrucks.com

Image Source: Company, www.tornadotrucks.com

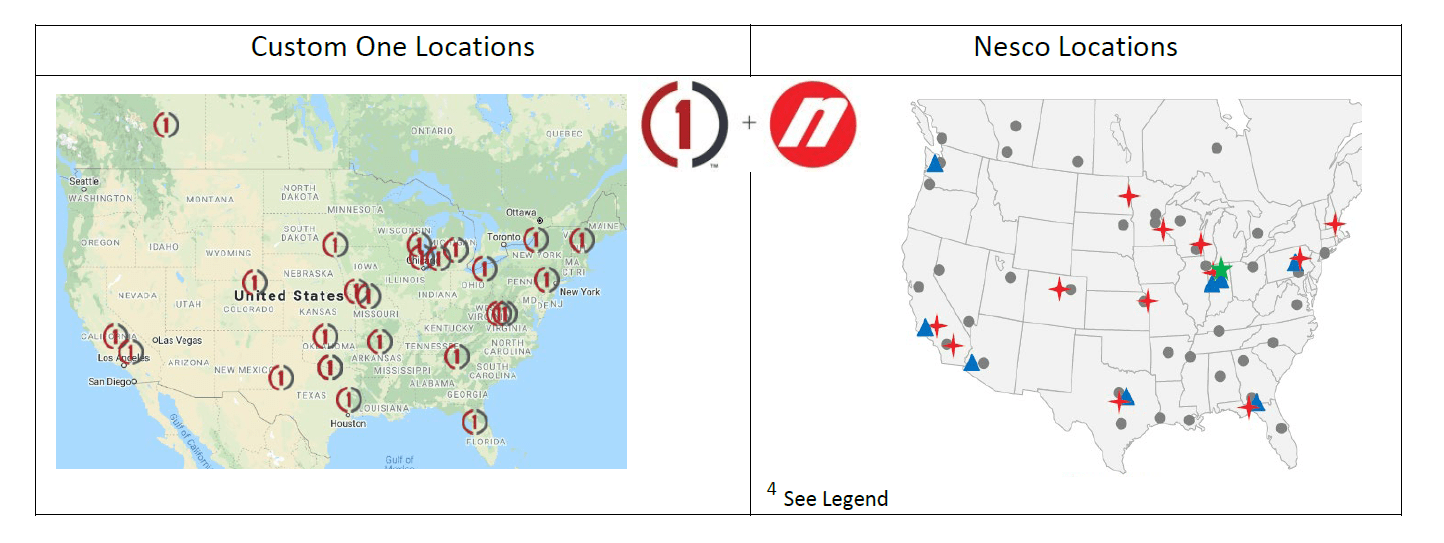

Leading and Well-Financed Distribution Partner

In April of 2018, Tornado entered a strategic alliance with Custom Truck One Source for the US distribution of Tornado’s products along with parts and services throughout all its locations. Custom Truck is a leading provider of specialized truck and heavy equipment solutions to the utility, rail, infrastructure, and telecommunications markets in North America.

On April 1, 2021, Custom Truck was acquired for $1.475 billion by Nesco Specialty Rentals, another leader in the industry focused significantly on utilities and utility contractors, with an equity investment of $850 million by Platinum Equity (a previous Nesco owner) and $100 million from existing shareholders Blackstone Group, Energy Capital Partners and Capitol Investment. “We believe the new company will be distinctively well-positioned to take advantage of the anticipated growth in critical U.S. infrastructure efforts in energy, telecom and rail over the near term and beyond,” said Mark Ein, Vice Chairman of Nesco Holdings, upon announcement of the deal in December 2020.

“The combined company’s increased scale and national presence will provide significant opportunities to further penetrate new and existing customers across geographies and end-markets serving highly attractive and growing infrastructure end markets, including the transmission and distribution energy grid, the 5G revolution build-out and critical rail and other national infrastructure initiatives.”

The Custom One/Nesco merger has nearly doubled the distribution reach from 26 to 46 company-operated locations. Headquarters remain in Kansas City with Fred Ross as CEO of the combined entity.

Image Source: Company Press Release and https://www.customtruck.com/locations/

Tornado Hydrovacs Growth in the Municipal Market

Introduction of the F2 line (7 yards3 debris, 800 gallons water capacity) for city markets will be a great complement to popular F3, F4 and F5 Eco-Lite lines (10-12 yards3 debris, 1,250-1,950 gallons water). Competitor units range from 6 to 15 yards3 debris bodies with prices ranging from $350,000 to $500,000.

With a concentration of sales in the mid-west U.S., Tornado has plans to expand its product reach with the adding of additional regional hydrovac distributors that have shown great interest in selling the company’s industry leading hydrovacs to the municipal market.

Growth and Value Opportunity Going Forward

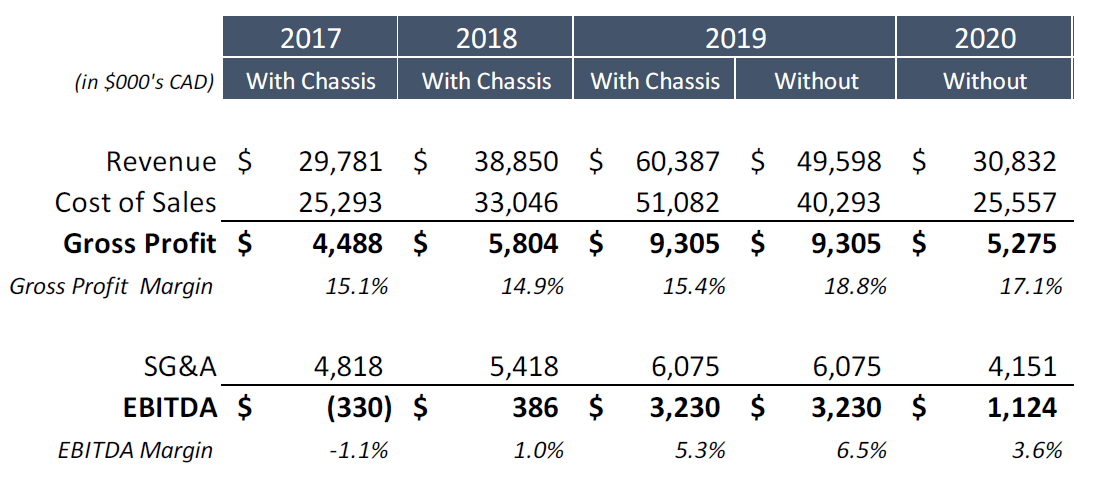

Tornado’s Historical Financials: Tornado had been making significant strides into the U.S. market leading up to the Covid-19 pandemic. Revenue in the U.S. more than doubled from 2018 to 2019 and accounted for 55% of total sales. The company weathered the 2020 pandemic with earnings slightly above those of 2018 but naturally our projections expect a return to growth as the U.S. continues its recovery. (Please note that 2017 and 2018 figures include the same amount in revenues and costs for the chassis sold as part of hydrovac units; 2019 figures were restated and show “With Chassis”. From 2020 onward, filings will include only Tornado product sales)

Chart Source: Personally Created in Excel Based on Company Filings

In 2020, we did see Tornado’s highest ever sales figures from Parts and Services, with a $4 million revenue contribution. This is an area of the business that the new Red Deer facility will help continue to grow as its central location and multi-bay facility can be extremely well utilized with all types of trucks requiring parts and services.

Projections and Initial Valuation Views: This year, 2021, will still be a post-Covid-19 transition year, with perhaps H2 2021 reflecting a steady increase of traditional U.S.-destined production at the new facility as a healthy economic recovery demand comes back. Based on direct manufacturing costs in 2019 and overall cost of sales margin improvements with increased revenue at the new facility, we project the following for 2021 through 2023. (2021 and 2022 conservatively assumes $4 million in Parts & Services sales and an increase to $5 million in 2023.)

Chart Source: Personally Created in Excel Based on Personal Projections

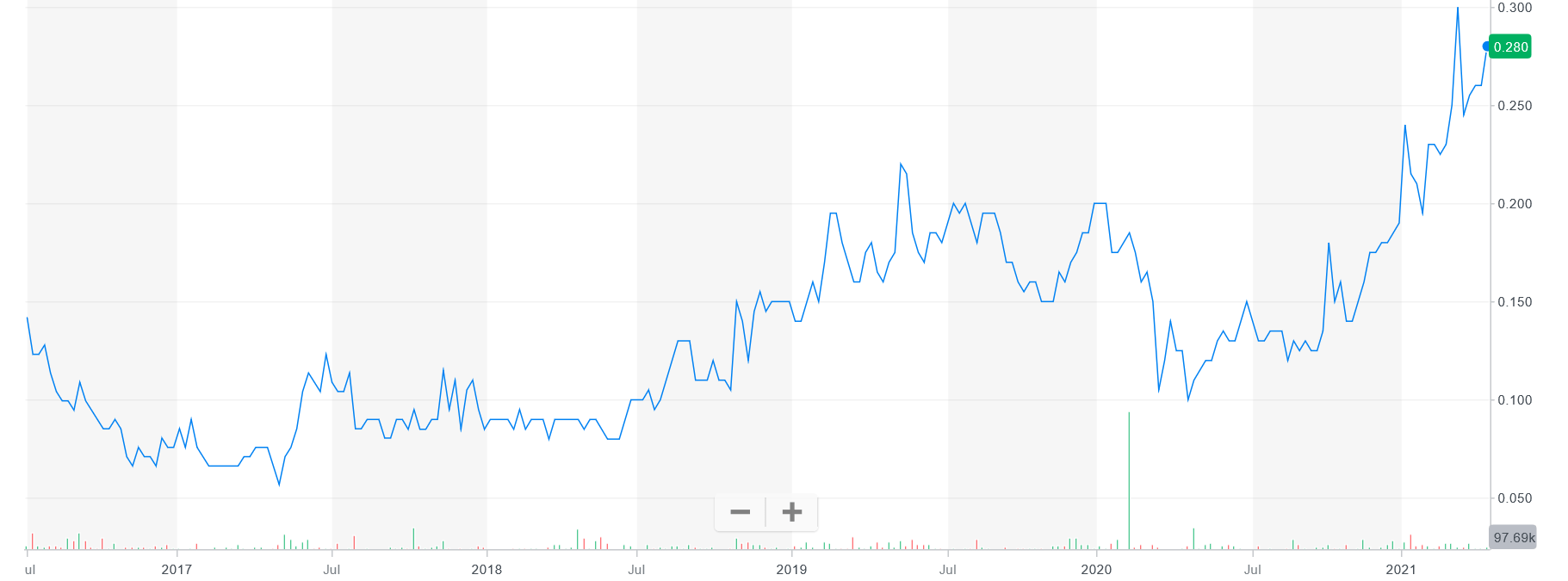

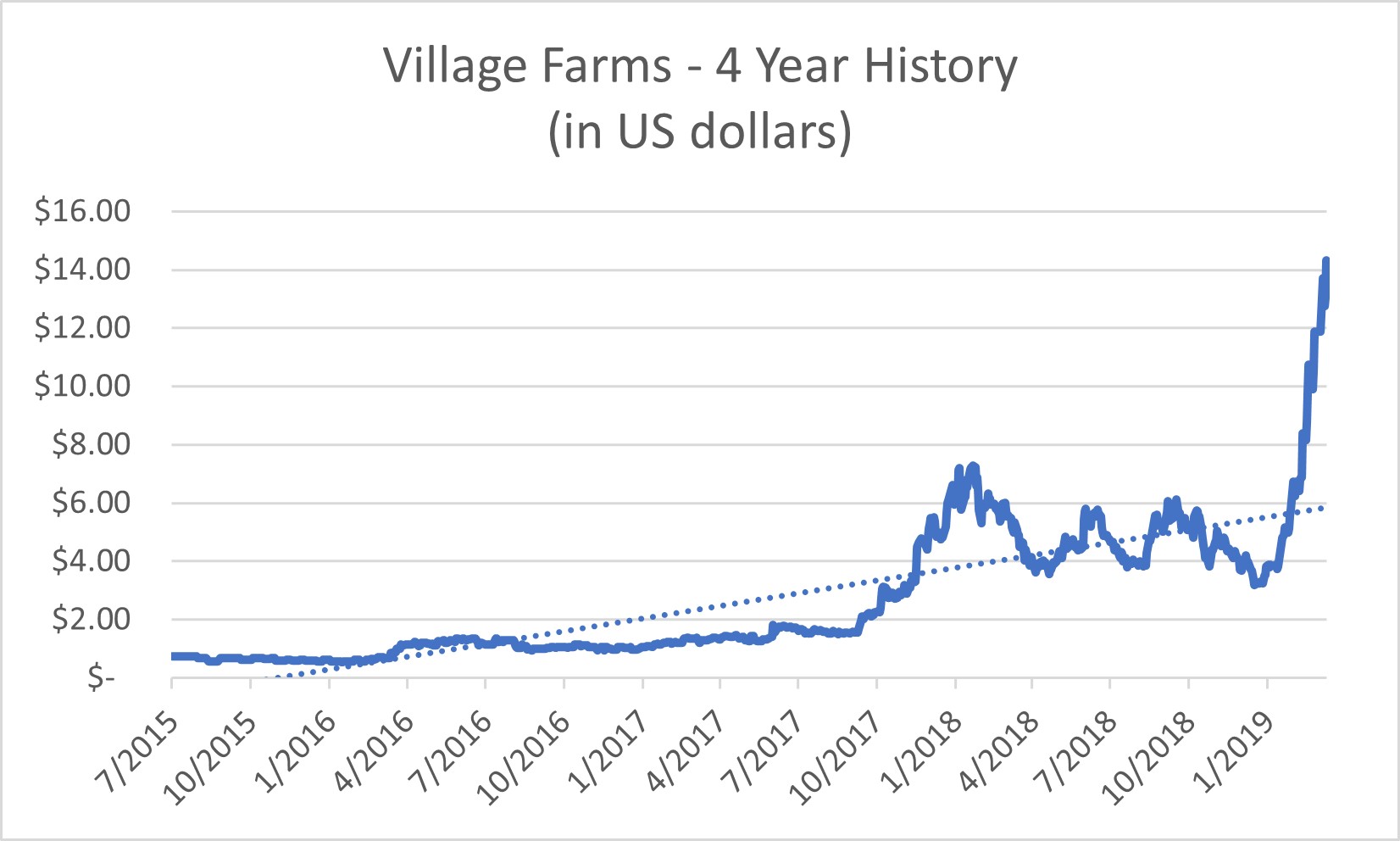

Tornado’s Stock Performance

Since going public at the end of June 2016, Tornado has remained below $0.45 a share. Over the past five years the company has fine-tuned its design and manufacturing to produce leading offerings for the North American hydrovacs industry. With the new facility in Red Deer, Alberta, increased manufacturing and service capacity, tremendous projected demand and a major U.S. distribution partner, we think this stock is an opportunity for impressive returns and should approach $1.50 per share.

The company currently trades at 38.3x 2020 EBITDA. Badger Infrastructure Solutions Ltd., a larger cap leader in the industry that we discussed earlier, trades at 15.7x 2020 EBITDA. Based on our projections, we expect EBITDA to consistently increase over the coming quarters and approach $15 million for year-end 2023. Assuming an EBITDA multiple of just 13x for 2023 EBITDA, we would exceed our $1.50 per share expectation based on the valuation specifics discussed.

![]()

Image Source: Yahoo! Finance Stock Chart

Image Source: Yahoo! Finance Stock Chart

Experienced Management Team Well-Aligned with Major Shareholders

The company has an experienced management team and board of directors led by CEO Bill Rollins, Non-Executive Chairman Guy Nelson, and the largest shareholder James Chui (41% of common shares). Mr. Chui purchased his equity in 2016 and 2017 at an average price of $0.20 per share. The company recently hired Brett Newton, a hydrovac industry leader. Brett served as Vice President of Operations and Fleet Manager for Badger franchises in Toronto, Hamilton and Niagara, before creating his own hydrovac service operation in Ontario. For the past five years, he has been a co-founding partner of Rival Hydrovac, a competitor to Tornado. Rival sold almost 500 hydrovacs into the municipal market in the past five years.

Along with Mr. Chui’s 52 million shares, Mr. Nelson, Mr. Rollins and Mr. Newton have shares and options for an additional 9 million shares; company insiders combined own close to half of all outstanding shares on a fully diluted basis.

The Parts and Services team is led by John Lavoie, an experienced operator in the hydrovac industry who previously worked at Clean Harbors before coming to Tornado. Since 2016, Rich Konkler has overseen sales in the United States and the partnership with Custom One.

Thinking About Electric

Tornado’s engineers have excelled in making their hydrovac trucks able to carry more payload with lighter manufacturing materials to the benefit of operators. As the electrification of commercial vehicles in North America progresses, Tornado’s engineering expertise and relationships with chassis manufacturers will be a great advantage. Utilizing battery technology with high energy density systems to power components like the blower, water pump and water heater systems on hydrovac trucks will be key if the cost-efficient electrification of future vehicle development becomes an operator preference.

Risks

Future growth is a key part of the share price increase that we project. There are a number of negative events, that if they were to take place, would surely impede the ability for the type of revenue and EBITDA improvement that we have discussed.

- Should bipartisan negotiations around the proposed “American Jobs Plan” fall apart and result in a major reduction of the $386 billion in hydrovac-friendly initiatives, the company would lose revenue opportunities.

- The newly opened manufacturing facility in Red Deer, Alberta, is expected to be able to produce up to 240 units annually. If it is unable to do so, and customers need to shift their orders elsewhere, the company would lose revenue opportunities. This facility is also projected to be a hub for parts and services for the entire region. If customers do not bring their business to the Red Deer facility, the company would lose revenue opportunities.

- The hydrovacs industry is competitive, with multiple companies providing trucks. Mergers between smaller competitors could create economies of scale and market reach that might increase the overall competition faced by the company, above and beyond what it is already dealing with. Badger, the largest company in the industry, might expand its operations even further than already planned and create ongoing pressure.

- Covid-19 had a significant effect on the company’s earnings. If the pandemic returns to peak economic disruption, earnings would once again be significantly affected.

- Lastly, if the electrification of commercial vehicles in North America far exceeds current expectations and municipalities prefer only electrified vehicles, the company will need to integrate production and engineering changes to its vehicles much faster than we have anticipated.

Additional disclosure: Disclaimer

Opinions and estimates offered constitute our judgment and are subject to change without notice, as are statements of financial market trends, which are based on current market conditions. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. This material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The views and strategies described may not be suitable for all investors. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, accounting, legal, tax advice, or investment matters and readers are advised to consult their own professional advisers. Any forecasts contained herein are for illustrative purposes only and are not to be relied upon as advice or interpreted as a recommendation.

First Bridge Investment Group does not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise. Any discussion in this document of past or proposed outcomes should not be relied upon as any indication of future outcomes. First Bridge Investment Group does not have any duty to you, whether in contract, tort, under statute or otherwise with respect to or in connection with this publication or the information contained within it. To the fullest extent permitted by law, First Bridge Investment Group disclaims any responsibility to liability to for any loss or damage suffered or cost incurred by you or by any other person arising out of or in connection with you or any other person’s reliance on this publication or on the information contained within it and for any omissions or inaccuracies.

Editor’s Note: This article covers one or more stocks trading at less than $1 per share and/or with less than a $100 million market cap. Please be aware of the risks associated with these stocks.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}